Code of Corporate Governance

Annual review of governance

Introduction

Good corporate governance is fundamental to Maidstone Borough Council’s ability to lead the borough effectively, deliver high-quality services, safeguard public resources, and act in the best interests of residents, businesses, and other stakeholders.

Corporate governance describes the systems, processes, cultures, and values by which the Council is directed and controlled, and through which it accounts to, engages with, and, where appropriate, provides leadership to its communities. It is about ensuring that the Council is doing the right things, in the right way, for the right people, in a timely, inclusive, open, honest, and accountable manner.

This Local Code of Corporate Governance sets out the framework through which Maidstone Borough Council gives effect to the principles of good governance. It is based on the CIPFA/SOLACE Delivering Good Governance in Local Government Framework (2016) and reflects the seven core principles that underpin good governance in the public sector.

The Code brings together, in one place, the key governance arrangements, behaviours, and sources of assurance that demonstrate how the Council applies these principles in practice. While the Code describes the Council’s governance framework, it is the effective operation of these arrangements, supported by a strong organisational culture, that provides assurance of good governance.

The Local Code supports the Council’s commitment to continuous improvement and provides a clear basis for:

- decision-making and accountability;

- oversight, scrutiny and assurance; and

- transparent reporting to Members, auditors, regulators and the public.

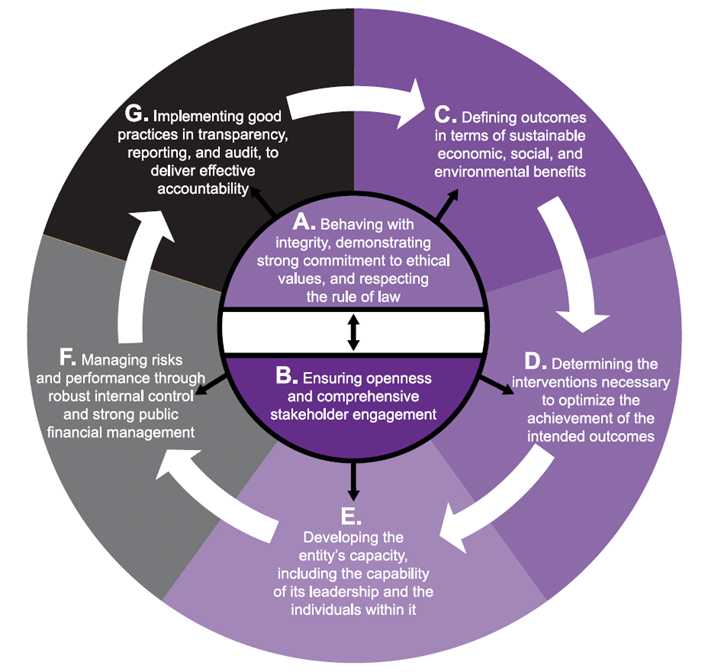

Code of Corporate Governance diagram

The image below shows how core principles (A and B) influence the cycle of governance (C through G).

- A. Behaving with integrity, demonstrating strong commitment to ethical values, and respecting the rule of law.

- B. Ensuring openness and comprehensive stakeholder engagement.

- C. Defining outcomes in terms of sustainable economic, social, and environmental benefits.

- D. Determining the interventions necessary to optimise the achievement of the intended outcomes.

- E. Developing the entity's capacity, including the capability of its leadership and the individuals within it.

- F. Managing risks and performance through robust internal control and strong public financial management.

- G. Implementing good practices in transparency, reporting, and audit, to deliver effective accountability.

Status, ownership, and review

This Local Code of Corporate Governance is a core component of Maidstone Borough Council’s overall governance and assurance framework. It underpins the Council’s statutory Annual Governance Statement, which is published alongside the Statement of Accounts and provides an annual assessment of the effectiveness of the Council’s governance arrangements.

The Code applies to:

- all Members of the Council;

- all officers; and

- governance arrangements relating to partnerships, shared services and other delivery arrangements where the Council has responsibility or accountability

Responsibility for maintaining and embedding the Code sits with the Council’s statutory officers and senior management, working collectively to ensure that governance arrangements remain robust, proportionate and effective.

The effectiveness of the Council’s governance framework, as set out in this Code, is reviewed annually. This review:

- assesses the extent to which the principles of good governance have been applied;

- considers evidence from internal and external sources of assurance, including audit, scrutiny and performance reporting; and

- identifies any governance issues or areas for improvement

The outcome of the annual review informs the preparation of the Annual Governance Statement, including any action plan required to address identified weaknesses or to strengthen governance arrangements further.

The Code itself is reviewed annually and updated as necessary to reflect:

- changes in legislation or statutory guidance;

- developments in best practice in local government governance; and

- changes to the Council’s governance structures or operating environment

Oversight of the Code and the Annual Governance Statement is provided through the Council’s established audit and governance arrangements, ensuring appropriate Member scrutiny and independent challenge.

Annual review and reporting

To comply with the principles of good governance, we must ensure that systems and processes are continually monitored and kept up to date. An annual review of the Council’s Corporate Governance arrangements will be carried out using the guidance contained in the CIPFA/SOLACE Framework.

The purpose of the review will be to provide assurance that governance arrangements are adequate and operating effectively, or to identify action that is planned to ensure effective governance in the future. The results of the review will take the form of an Annual Governance Statement prepared on behalf of the Leader of the Council and the Chief Executive. It will be submitted to the Audit, Governance and Standards Committee for consideration and review.

Annual review of governance

Our actions and behaviours

Principle A - Behaving with integrity, demonstrating strong commitment to ethical values, and respecting the rule of law

| Sub principle | Actions and behaviours | Evidence |

|---|---|---|

| Behaving with Integrity |

|

|

| Demonstrating strong commitment to ethical values |

|

|

| Respecting the rule of law |

|

|

Principle B - Ensuring openness and comprehensive stakeholder engagement

| Sub principle | Actions | Evidence |

|---|---|---|

| Openness |

|

|

| Engaging comprehensively with institutional stakeholders |

|

|

| Engaging stakeholders effectively, including individual citizens and service users |

|

|

Principle C - Defining outcomes in terms of sustainable economic, social, and environmental benefits

| Sub principle | Actions | Evidence |

|---|---|---|

| Defining Outcomes |

|

|

| Sustainable economic, social and environmental benefits |

|

|

Principle D – Determining the interventions necessary to optimise the achievement of the intended outcomes

| Sub principle | Actions | Evidence |

|---|---|---|

| Determining interventions |

|

|

| Planning interventions |

|

|

| Optimising achievement of intended outcomes |

|

|

Principle E - Developing the entity’s capacity, including the capability of its leadership and the individuals within it

| Sub principle | Actions | Evidence |

|---|---|---|

| Developing the entity’s capacity |

|

|

| Developing the capability of the entity’s leadership and other individuals |

|

|

Principle F - Managing risks and performance through robust internal control and strong public financial management

| Sub principle | Actions | Evidence |

|---|---|---|

| Managing Risk |

|

|

| Managing Performance |

|

|

| Robust Internal Control |

|

|

| Managing Data |

|

|

| Strong public financial management |

|

|

Principle G – Implementing good practices in transparency, reporting, and audit to deliver effective accountability

| Sub principle | Actions | Evidence |

|---|---|---|

| Implementing good practice in transparency |

|

|

| Implementing good practices in reporting |

|

|

| Assurance and effective accountability |

|

|